The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how gig economy stocks fared in Q4, starting with Angi (NASDAQ:ANGI).

The iPhone changed the world, ushering in the era of the “always-on” internet and “on-demand” services - anything someone could want is just a few taps away. Likewise, the gig economy sprang up in a similar fashion, with a proliferation of tech-enabled freelance labor marketplaces, which work hand and hand with many on demand services. Individuals can now work on demand too. What began with tech-enabled platforms that aggregated riders and drivers has expanded over the past decade to include food delivery, groceries, and now even a plumber or graphic designer are all just a few taps away.

The 6 gig economy stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 13% since the latest earnings results.

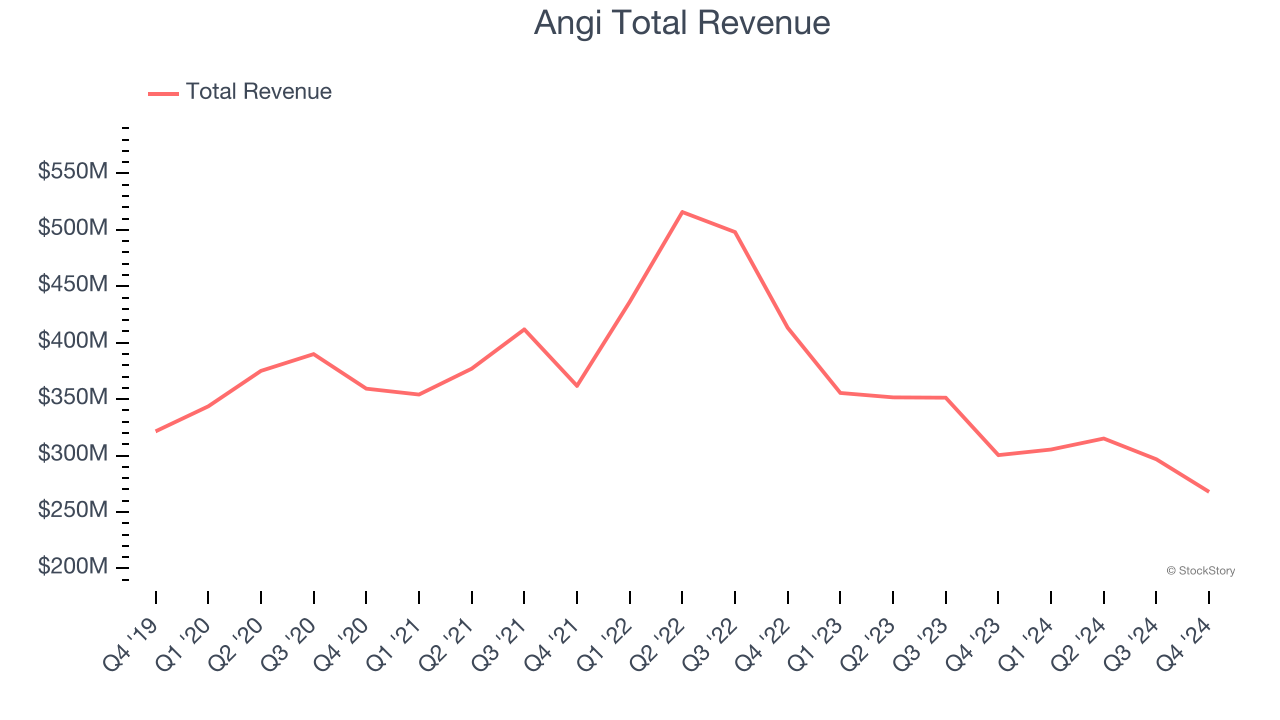

Best Q4: Angi (NASDAQ:ANGI)

Created by IAC’s mergers of Angie’s List and HomeAdvisor, ANGI (NASDAQ: ANGI) operates the largest online marketplace for home services in the US.

Angi reported revenues of $267.9 million, down 10.8% year on year. This print exceeded analysts’ expectations by 5.3%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ number of service requests estimates.

Angi delivered the slowest revenue growth of the whole group. The company reported 3.63 million service requests, down 16.1% year on year. Unsurprisingly, the stock is down 11% since reporting and currently trades at $1.53.

Is now the time to buy Angi? Access our full analysis of the earnings results here, it’s free.

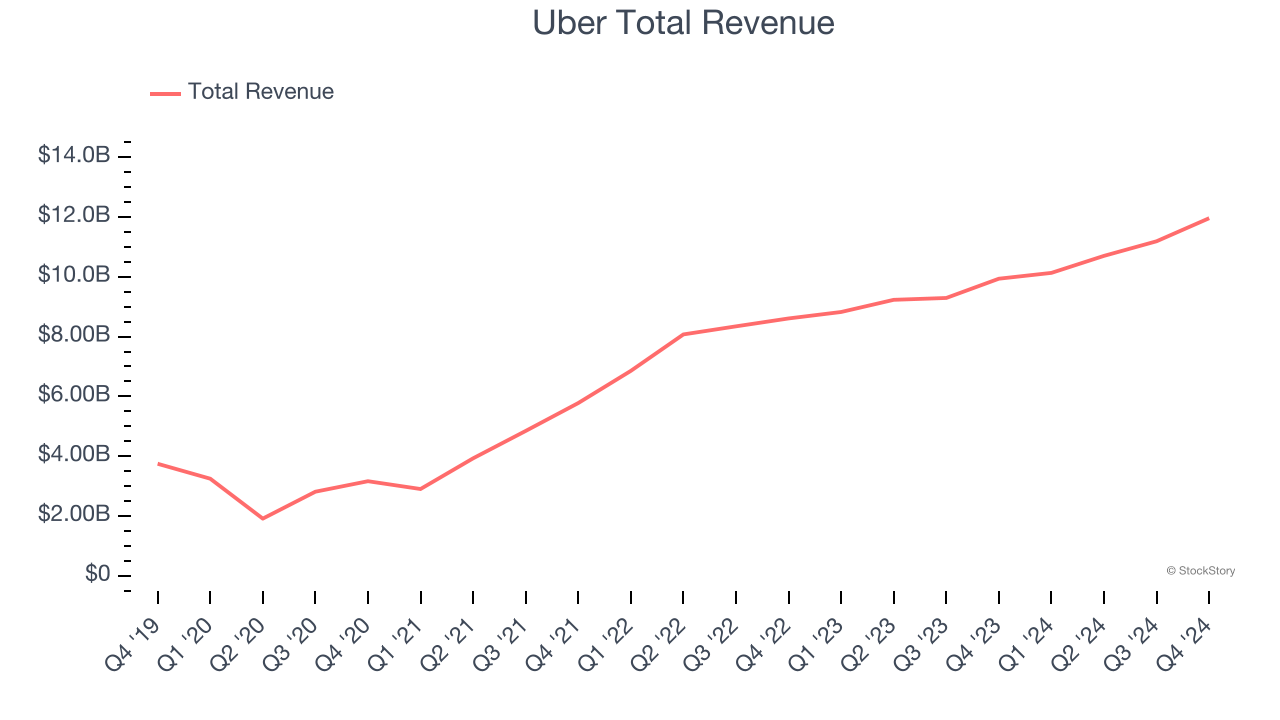

Uber (NYSE:UBER)

Notoriously funded with $7.7 billion from the Softbank Vision Fund, Uber (NYSE:UBER) operates a platform of on-demand services such as ride-hailing, food delivery, and freight.

Uber reported revenues of $11.96 billion, up 20.4% year on year, outperforming analysts’ expectations by 1.6%. The business had a satisfactory quarter with strong growth in its users but EBITDA in line with analysts’ estimates.

The market seems content with the results as the stock is up 1% since reporting. It currently trades at $70.47.

Is now the time to buy Uber? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Fiverr (NYSE:FVRR)

Based in Tel Aviv, Fiverr (NYSE:FVRR) operates a fixed price global freelance marketplace for digital services.

Fiverr reported revenues of $103.7 million, up 13.3% year on year, exceeding analysts’ expectations by 2.3%. Still, it was a slower quarter as it posted a decline in its buyers and EBITDA guidance for next quarter missing analysts’ expectations.

As expected, the stock is down 21.5% since the results and currently trades at $25.99.

Read our full analysis of Fiverr’s results here.

Upwork (NASDAQ:UPWK)

Formed through the 2013 merger of Elance and oDesk, Upwork (NASDAQ:UPWK) is an online platform where businesses and independent professionals connect to get work done.

Upwork reported revenues of $191.5 million, up 4.1% year on year. This result beat analysts’ expectations by 5.8%. Aside from that, it was a mixed quarter as it also logged EBITDA guidance for next quarter exceeding analysts’ expectations but a significant miss of analysts’ number of gross services volume estimates.

Upwork scored the biggest analyst estimates beat but had the weakest full-year guidance update among its peers. The company reported 832,000 active customers, down 2.2% year on year. The stock is down 19.1% since reporting and currently trades at $12.58.

Read our full, actionable report on Upwork here, it’s free.

DoorDash (NASDAQ:DASH)

Founded by Stanford students with the intent to build “the local, on-demand FedEx", DoorDash (NYSE:DASH) operates an on-demand food delivery platform.

DoorDash reported revenues of $2.87 billion, up 24.8% year on year. This print surpassed analysts’ expectations by 1.1%. More broadly, it was a mixed quarter as it also produced strong growth in its requests but EBITDA guidance for next quarter slightly missing analysts’ expectations.

The company reported 685 million service requests, up 19.3% year on year. The stock is down 6.5% since reporting and currently trades at $180.50.

Read our full, actionable report on DoorDash here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.