As the Q2 earnings season wraps, let’s dig into this quarter’s best and worst performers in the consumer subscription industry, including Udemy (NASDAQ:UDMY) and its peers.

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

The 8 consumer subscription stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 1.2% on average since the latest earnings results.

Udemy (NASDAQ:UDMY)

With courses ranging from investing to cooking to computer programming, Udemy (NASDAQ:UDMY) is an online learning platform that connects learners with expert instructors who specialize in a wide range of topics.

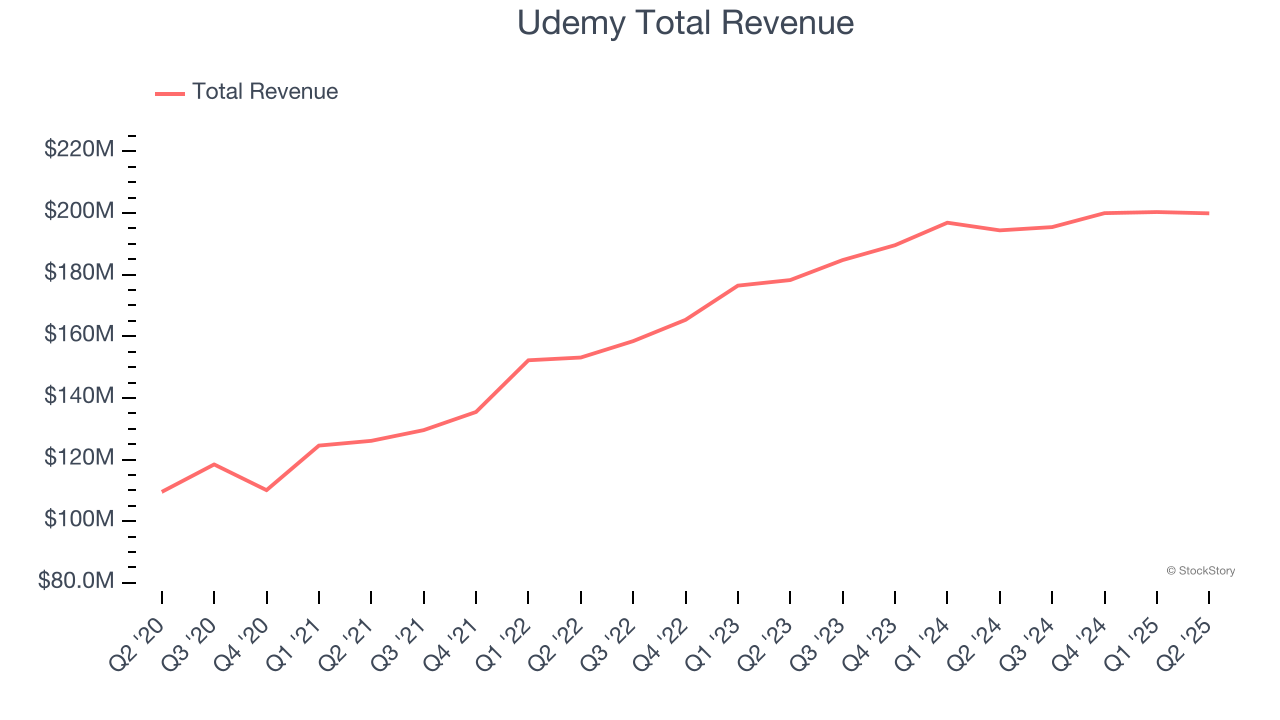

Udemy reported revenues of $199.9 million, up 2.8% year on year. This print exceeded analysts’ expectations by 1.5%. Overall, it was a satisfactory quarter for the company with an impressive beat of analysts’ EBITDA estimates.

"Our second quarter results mark an inflection point in Udemy's evolution, as we delivered both GAAP profitability and made meaningful progress on our strategy to drive accelerated growth,” said Hugo Sarrazin, President and CEO of Udemy.

Udemy delivered the weakest full-year guidance update of the whole group. The company reported 17,107 active buyers, up 3.1% year on year. The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $7.05.

Is now the time to buy Udemy? Access our full analysis of the earnings results here, it’s free.

Best Q2: Roku (NASDAQ:ROKU)

With a name meaning six in Japanese because it was the founder's sixth company that he started, Roku (NASDAQ: ROKU) makes hardware players that offer access to various online streaming TV services.

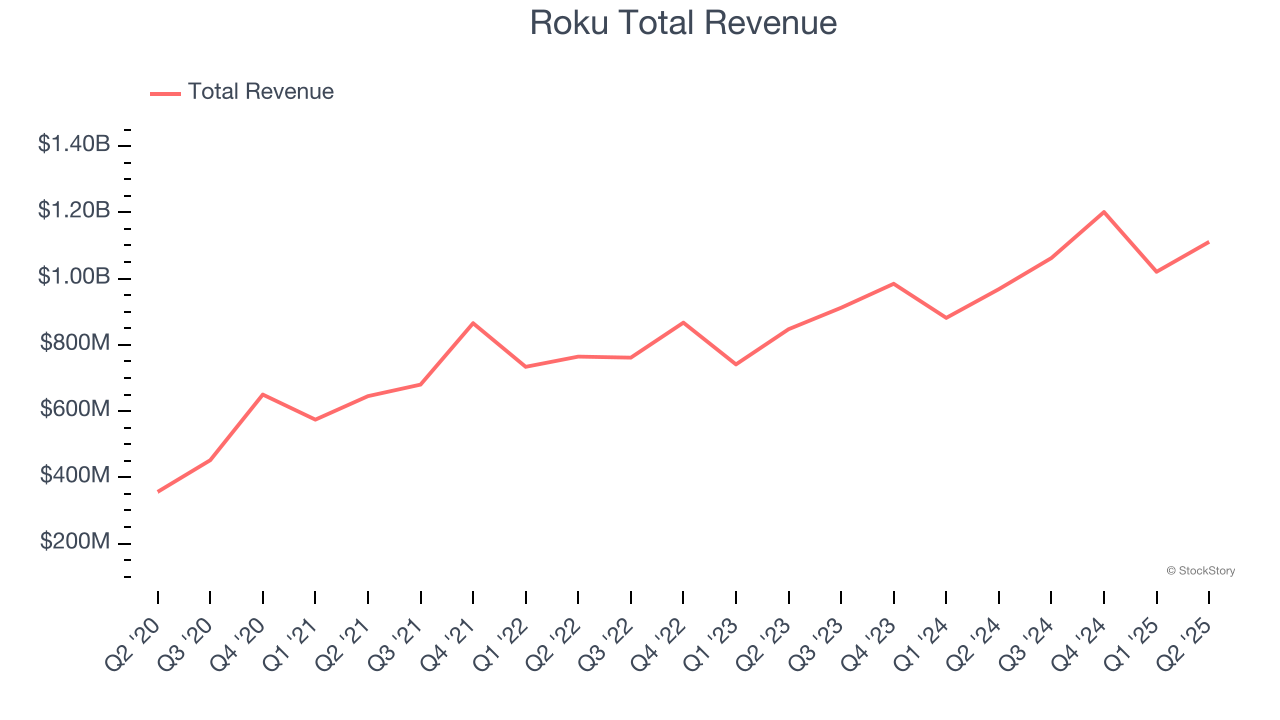

Roku reported revenues of $1.11 billion, up 14.8% year on year, outperforming analysts’ expectations by 3.8%. The business had a very strong quarter with an impressive beat of analysts’ EBITDA estimates and full-year EBITDA guidance exceeding analysts’ expectations.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 11.6% since reporting. It currently trades at $83.31.

Is now the time to buy Roku? Access our full analysis of the earnings results here, it’s free.

Slowest Q2: Match Group (NASDAQ:MTCH)

Originally started as a dial-up service before widespread internet adoption, Match (NASDAQ:MTCH) was an early innovator in online dating and today has a portfolio of apps including Tinder, Hinge, Archer, and OkCupid.

Match Group reported revenues of $863.7 million, flat year on year, exceeding analysts’ expectations by 1.2%. Still, it was a softer quarter as it posted a decline in its users

Interestingly, the stock is up 7.1% since the results and currently trades at $36.10.

Read our full analysis of Match Group’s results here.

Coursera (NYSE:COUR)

Founded by two Stanford University computer science professors, Coursera (NYSE:COUR) is an online learning platform that offers courses, specializations, and degrees from top universities and organizations around the world.

Coursera reported revenues of $187.1 million, up 9.8% year on year. This result surpassed analysts’ expectations by 3.7%. It was a very strong quarter as it also logged EBITDA guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ EBITDA estimates.

Coursera pulled off the highest full-year guidance raise among its peers. The company reported 183 million active customers, up 18% year on year. The stock is up 37.1% since reporting and currently trades at $12.45.

Read our full, actionable report on Coursera here, it’s free.

Chegg (NYSE:CHGG)

Started as a physical textbook rental service, Chegg (NYSE:CHGG) is now a digital platform addressing student pain points by providing study and academic assistance.

Chegg reported revenues of $105.1 million, down 35.6% year on year. This number topped analysts’ expectations by 3.8%. Taking a step back, it was a slower quarter as it produced a significant miss of analysts’ number of services subscribers estimates.

Chegg had the slowest revenue growth among its peers. The company reported 2.62 million users, down 39.9% year on year. The stock is down 9.4% since reporting and currently trades at $1.16.

Read our full, actionable report on Chegg here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.